The $20B Problem Airlines Can Solve Today: Payment Orchestration

Overview

In 2022, global airlines spent over $20.3 billion on payment processing — a figure that exceeds 50% of the industry’s total net profits. That means for every dollar of profit made, nearly another was lost to transaction fees, fraud, chargebacks, and inefficiencies.

Margins in aviation have always been razor-thin. But with rising costs, lingering post-COVID recovery challenges, and geopolitical instability, airlines can no longer afford to overlook the hidden costs buried in their payment stack.

The good news? Payment orchestration — once seen as a technical afterthought — is now a strategic lever. It’s one of the few areas where executives can still unlock meaningful cost savings, improve customer experience, and meet upcoming compliance requirements (like PCI DSS v4.0) without massive operational risk.

Below, we’ll break down exactly how much revenue is lost in payment operations today, and why CEOs, CFOs, and CTOs should start treating payment orchestration as a board-level priority.

The Hidden Profit Drain: How Payments Consume Half Your Bottom Line

The airline industry's profitability paradox becomes clear when examined through the payment lens. IATA projects that airlines will serve a record 4.99 billion travelers in 2025, generating impressive top-line growth. Yet this revenue success masks a fundamental challenge: the industry's structural inability to convert revenue into sustainable profits.

The numbers are sobering. The global airline industry's expected net profit of $36 billion translates to just 3.7% net profit margin—roughly half the profitability achieved across other industries. Within this constrained environment, payment acceptance costs represent a massive drain that most executives underestimate.

.png)

A landmark study by Edgar, Dunn & Company, commissioned by IATA, quantified the industry's payment burden at $20.3 billion annually. This translates to 2.1% of total revenue being consumed simply by collecting payment from customers. Consulting firm Globant corroborates this analysis, citing an average Merchant Discount Rate (MDR) for airlines of 2.5% of transaction value.

The strategic implications are staggering. Payment costs aren't a rounding error—they represent direct erosion of potential profits. When compared to the industry's projected 36 billion in global net profit, 20+ billion in payment costs reveals that processing transactions consumes more than 56% of the industry's hard-won profits.

This reframes payment optimization entirely. A payment partner capable of reducing processing costs by just 10% would contribute over $2 billion directly back to industry bottom lines—potentially increasing net profits by more than 5% across the sector.

The situation is compounded by structural constraints that limit traditional growth strategies. McKinsey's 2025 analysis highlights a global deficit of roughly 2,000 aircraft due to pandemic-era production slowdowns and ongoing supply chain disruptions.

This capacity constraint means airlines cannot simply add more flights to grow revenue. The primary path to improved profitability lies in increasing the margin on each ticket sold using existing fleet capacity.

Conversion Losses You Can't Afford: The Revenue Bleeding You Don't See

Beyond direct processing costs, a more insidious problem undermines airline profitability: failed conversions. Airline websites consistently face some of the highest cart abandonment rates in e-commerce — often exceeding 80%. And a significant share of those drop-offs happen at the payment stage.

.png)

The revenue impact is staggering. For an airline processing 10 million bookings annually at an average value of €400, a modest 5% drop in conversion due to payment friction equates to €200 million in lost revenue every year.

This isn’t theoretical — it’s happening right now on booking funnels across the industry.

The Local Payment Method Advantage

Payment preferences vary dramatically by geography, and airlines that ignore these differences pay a steep price. In Germany, for example, SOFORT and giropay dominate online payments. In the Netherlands, iDEAL commands over 60% market share. Scandinavian customers prefer Klarna and other regional solutions.

Airlines offering only international card brands in these markets face conversion rates 10-20% lower than competitors providing local payment options. For a mid-sized European carrier processing €500 million in bookings, adding comprehensive local payment support could generate €25-50 million in additional revenue annually.

Multi-Acquiring: The Approval Rate Game-Changer

Traditional single-acquirer setups create a hidden point of failure. If one payment processor declines or experiences latency, the transaction fails — and so does the customer’s booking.

Modern payment orchestration platforms eliminate this risk by dynamically routing transactions across multiple acquirers in real-time, significantly improving approval rates.

The gains are measurable. Paybyrd’s internal analysis shows uplift of:

- +1.72% vs. Adyen

- +3.16% vs. Elavon

- +4.86% vs. Checkout.com

- +4.92% vs. Nuvei

At scale, even modest improvements drive major upside. Consider this: for an airline processing €1 billion in annual bookings, a 3% approval rate increase adds €30 million in recovered revenue. With industry margins hovering around 3–4%, that alone could boost net profits by 25% or more.

The BNPL Opportunity

Buy Now, Pay Later (BNPL) and split payment solutions have gained significant traction, particularly for higher-value purchases like airline tickets. Air Europa's implementation provides a compelling case study—the airline reported €3.8 million in incremental revenue and €2.4 million in decline recovery through their partnership with Amadeus for flexible payment solutions.

The demographic implications are critical. Research indicates that 73% of Gen Z consumers have used or would consider using BNPL for travel purchases. Airlines that fail to accommodate these preferences risk losing market share to competitors offering more flexible payment terms.

.png)

Compliance Is Here: The March2025 Mandate

The regulatory landscape is shifting rapidly, and the deadlines are non-negotiable. The Payment Card Industry Data Security Standard (PCI DSS) version 4.0 became fully enforceable in March 2025, introducing mandatory security controls that many legacy systems cannot meet.

The stakes are existential. Unlike previous PCI DSS updates, version 4.0 includes mandatory security controls that cannot be compensated through alternative measures. Payment card networks can impose transaction restrictions, increase processing fees, or even terminate merchant agreements for non-compliant organizations. For airlines dependent on card-based payments, these sanctions could severely impact business operations and revenue generation.

The technical requirements are particularly challenging for airlines operating legacy payment systems. The new standard mandates enhanced encryption, improved access controls, regular security testing, and comprehensive audit trails. Many existing airline payment infrastructures lack the architectural foundation to support these requirements without significant overhaul.

European Regulatory Convergence

Simultaneously, the European Union's regulatory framework is creating both opportunities and obligations. The Instant Payments Regulation mandates that all payment service providers offer instant euro transfers by 2025. The upcoming PSD3/PSR frameworks are reshaping rules around fund settlement, consumer protection, and merchant liability.

These changes create opportunities for lower-cost, real-time payments while imposing significant risks for those unprepared. Early adopters can gain competitive advantage through lower costs and improved customer experience, while laggards risk being disadvantaged as instant payments become the expected standard.

Cash Flow Acceleration: Turning Working Capital Into Competitive Advantage

Airlines benefit from a rare cash flow advantage: they often receive payment weeks or months before delivering the service. But traditional card processing undermines this edge by introducing settlement delays of 1–3 business days, tying up millions in working capital.

The cost of that delay is real. For an airline processing €100 million in monthly bookings, a two-day lag effectively means giving €6.7 million in interest-free credit to payment processors. Over a year, that’s €80 million in delayed liquidity — capital that could otherwise be fueling fleet upgrades, fuel hedging, or operational optimization.

Modern real-time payment methods, like Account-to-Account (A2A) and SEPA Instant, change the game. These methods settle funds within seconds, unlocking strategic advantages:

- Improved treasury management — precise, real-time cash positioning

- Lower financing costs — less dependency on working capital loans

- Stronger fuel hedging — earlier access = better deal windows

- Greater agility — more flexibility to capitalize on market shifts

And the benefits aren’t just faster — they’re cheaper. A2A payments typically cost under 1%, compared to 2–3% for cards, delivering both margin improvement and cash flow acceleration in one move.

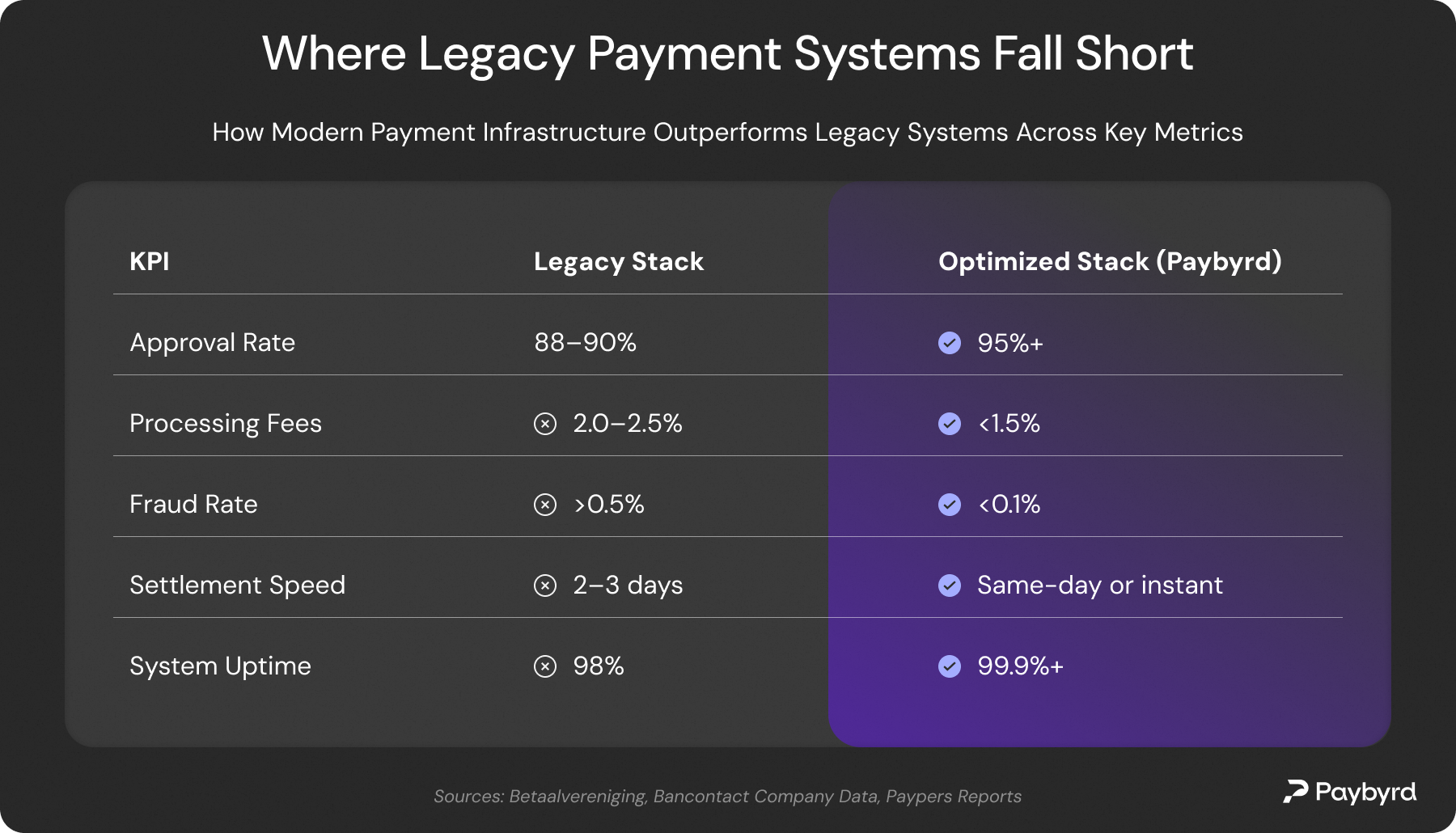

What Great Payment Performance Looks Like: The Benchmarks That Matter

Approval Rates

Leading platforms consistently exceed 95% approval for legitimate transactions. In contrast, many legacy systems struggle to reach 90%.

→ On €100 million in attempted bookings, that 5% difference equates to €5 million in recovered revenue.

Processing Costs

Top-performing providers achieve blended processing fees of under 1.5% of transaction value. The industry average still exceeds 2%.

→ For airlines processing billions in annual bookings, this cost delta translates to tens of millions in annual savings.

Processing Costs

Modern systems maintain fraud rates below 0.1%, while keeping false positives under 1%. Poor fraud management causes a double hit: lost revenue to fraud and lost revenue from mistakenly declined legitimate customers.

System Uptime

Enterprise-grade infrastructure ensures 99.9%+ uptime. Any downtime — even minutes — can mean millions in missed revenue during peak booking windows.

Settlement Speed

Best-in-class platforms enable same-day or instant settlement, unlike the traditional 2–3 business day cycles. Faster settlement improves working capital management and reduces the need for external financing.

How Paybyrd Transforms Airline Payment Performance

Paybyrd is purpose-built to meet the unique challenges of airline payments — from global scale and regulatory complexity to margin pressure and fragmented infrastructure. The platform delivers measurable improvements across every key performance area:

Superior Approval Rates

Paybyrd’s multi-acquiring engine routes each transaction to the optimal processor in real time, driving approval rate improvements of up to 4.92% compared to major providers. → For an airline processing €1 billion annually, that uplift equates to €30–50 million in additional confirmed bookings.

Optimized Costs

Advanced routing algorithms automatically select the most cost-efficient path for every transaction. Combined with support for low-cost Account-to-Account (A2A) payments and real-time settlement, this reduces overall processing costs and improves cash flow velocity.

Unified Operations

Paybyrd unifies payment logic, fraud prevention, and reporting into a single platform — streamlining operations and providing complete transparency across all geographies, channels, and payment methods.

Local Market Expertise

With deep support for local payment methods across European markets — including iDEAL, Bancontact, SEPA Instant, and more — Paybyrd helps airlines maximize conversion and approval rates in every market they serve.

The Strategic Imperative: From Cost Center to Competitive Advantage

For airline executives, payment optimization is no longer a technical upgrade — it’s a strategic lever. With payment costs now consuming more than half of the industry’s net profits, modernizing infrastructure offers one of the clearest paths to immediate and scalable ROI.The impact spans every financial lever:

- Lower processing costs unlock room for more competitive pricing or stronger margins

- Higher approval rates translate directly to topline revenue growth

- Faster settlement strengthens cash flow and treasury control

- Built-in compliance mitigates regulatory risk and reduces internal overhead

But the window of opportunity is narrowing. As the industry wakes up to the importance of payments, the advantage will go to first movers. Those who act now will capture disproportionate gains in profitability, agility, and customer experience.This is not just about infrastructure — it’s about positioning your airline for leadership. With PCI DSS v4.0 enforcement beginning in March 2025 and sweeping European payment regulations on the horizon, now is the time to act decisively.The question isn’t whether to modernize your payment stack. It’s whether you intend to lead — or be left behind.

The Strategic Imperative: From Cost Center to Competitive Advantage

Fraud prevention has evolved from a necessary expense to a strategic differentiator that directly impacts customer trust, operational efficiency, and financial performance. Businesses that invest in sophisticated fraud prevention capabilities gain multiple advantages:

Customer Trust: Robust security measures protect customer data and financial information, building trust that translates to increased loyalty and higher transaction values.

Operational Efficiency: Automated fraud detection reduces manual review requirements while improving transaction approval rates for legitimate customers.

Regulatory Resilience: Proactive compliance with evolving regulations like VoP and PSD3/PSR reduces regulatory risk while positioning businesses ahead of competitors.

Financial Performance: Reduced fraud losses, lower chargeback rates, and improved authorization rates directly impact bottom-line performance.

The window for competitive advantage is narrowing as regulatory requirements become mandatory and fraud sophistication increases. Early adopters of advanced fraud prevention technologies will capture disproportionate benefits while late movers face increased risks and compliance challenges.

The time for action is now. With VoP requirements becoming mandatory in October 2025 and fraud losses continuing to escalate, businesses must move quickly to implement comprehensive fraud prevention strategies.Ready to transform your fraud prevention capabilities? Contact Paybyrd to discover how our integrated platform can protect your business while improving customer experience.

Related Articles

.png)

Ready to take it to the next level?

Start right away, or get in touch for a no-obligation free consultation with one of our knowledgeable team members.